{kind=link}

BetterBond

The July BetterBond Property Brief reveals that BetterBond’s index shows a 7.4% year-on-year increase in applications for the 12 months to May 2025 – a positive indicator in a stabilising market, and well above the 2.8% CPI. It also notes that with inflation remaining below the Reserve Bank’s target, economists anticipate a further interest rate cut in July, which could further energise buyer activity.

The month in numbers

- 7.4% YOY increase in the number of home loan applications

- R1.28 million average house price for first-time buyers

- R165,000 average deposit for first-time buyers

- 13.6% YOY increase in home loans granted

BetterBond index of home loan applications

Despite a fairly active month in May, as well as a marginal decline in the prime lending rate, homebuying activity during Q2 2025 could not match the performance of Q1 2025.

Fortunately, however, the YOY increase in the number of home loan applications did manage to increase, with the bonus of an increase that outpaced the rise in the latest consumer price index (CPI), namely 7.4% (CPI was at merely 2.8% at the end of May). The residential property market still has a long way to go before breaching the levels of activity experienced at the beginning of 2021 – prior to the Monetary Policy Committee (MPC) embarking on a restrictive policy approach that saw the prime rate climb to a 15-year high.

The index for the 12 months ending in May 2025 is now 28% lower than four years ago. Fortunately, a measure of stability has returned to the residential property market, with the latest index reading 4.5% higher than two years ago. With the CPI remaining below the MPC’s target range for inflation, there is an excellent chance for another rate cut at the end of July.

Average home purchase price

After reaching an all-time high of R1.3 million during Q1 2025, the average house price for first-time buyers (FTBs) declined marginally to R1.28 million in Q2 2025.

The subdued level of activity in homebuying has manifested itself in YOY declines for all buyers and FTBs alike, both in nominal and real terms. During Q2 2025, the average house price for all buyers amounted to R1.58 million, confirming the continued presence of a buyer’s market for houses, as do the declines of 6.4% and 8.3%, for real house prices for all buyers and FTBs, respectively, since Q1 2022. After this date, the relentless rise in interest rates started to bite into the pockets of prospective homeowners.

With the debt service costs as a percentage of household income having moved rapidly from 6.7% in 2021 to 9.1% in 2024, the dampening effect on residential property market activity was no surprise. Fortunately, the latter has started to decline and is now at 8.9%

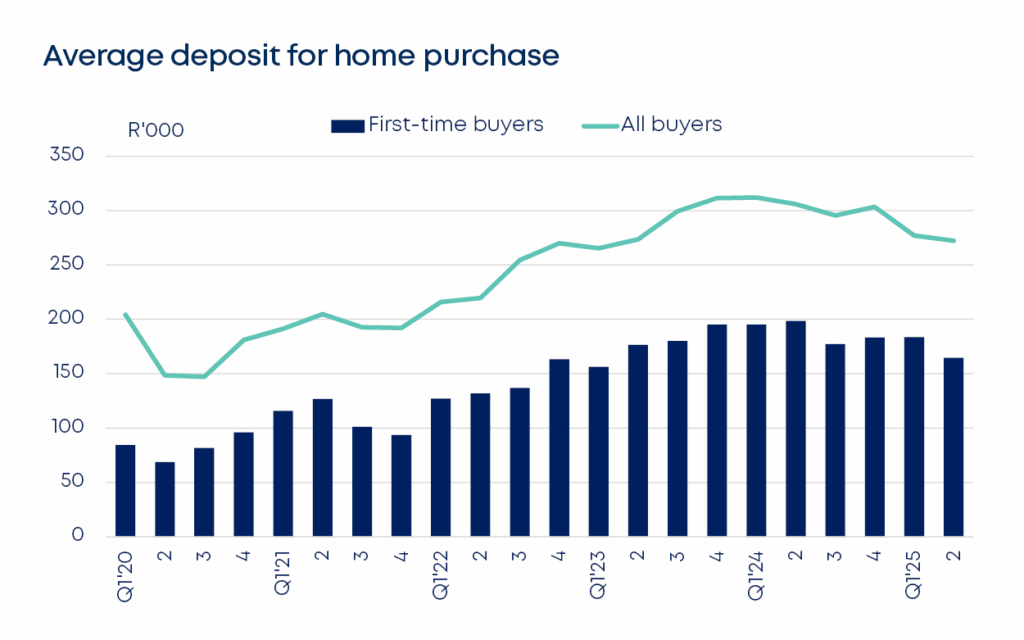

Average deposit for home purchase

During the first half of last year, the average deposits required for home loan approvals reached a peak, but this trend has now been reversed, with a YOY decline of 17% for FTBs and 11% for all buyers having been recorded in Q2 2025.

After moving to above R300,000 since the end of 2023, this value declined to an average of R272,000 during Q2 2025. FTBs have benefited even more, with a decline in the average deposit from just below R200,000 a year ago to R165,000 in Q2 2025. After a gradual increase until Q1 2024, the ratio of bank credit impairments to total bank assets has declined marginally to 2.5%. The deceleration in the growth of credit impairments at South African banks is a welcome development and confirms a high level of effective credit risk management.

Regional composition of home loans granted

Figure 4 illustrates the regional composition of home loans granted, with a YOY increase of 13.6%.

Reasons for this welcome trend include marginal interest rate relief, with the prime lending rate now at 10.75%, compared to 11.25% at the beginning of 2025. Although criticism has been levelled against the monetary policy authorities for not lowering interest rates at a faster pace, any lowering immediately raises the affordability of home purchases, especially for FTBs.

Another reason has been the declining trend of real home prices (after adjustment for inflation). Combined with sustained increases in real incomes of home loan applicants, this has also enhanced the attractiveness of buying a house. Johannesburg’s South-Eastern suburbs came in at number one for loans granted.

Percentage change in home loans granted by region (12 months to June 2024 & 2025)

Over the past 12 months, only two regions experienced a decline in the number of home loans granted, viz the Eastern Cape and Mpumalanga. Two other regions also under-performed relative to the rest of the regions and the national average increase of almost 14%, namely the North West and Johannesburg’s North-Western suburbs.

Greater Pretoria fared exceptionally well, with an increase in the number of home loans granted of 26.7%, possibly because of being home to the largest residential University in the country and also a number of motor vehicle manufacturers, which have spawned a large and diversified component manufacturing supply-chain. Predictably, the Western Cape continues to expand its home loan activity, with YOY growth of 14.7% for loans granted.

Read the full report here.